My favorite NFT PFP got LIQUIDATED...

My favorite NFT PFP got LIQUIDATED...

6 - The Review

RIP Sweet Prince

The NFT that I minted & became my brand for most of last year got liquidated over the weekend.

In a word: devastated.

My GhostKidDAO NFT has been with me since mint, through the start of the first ever SubDAO Twitter groupchat for Souls & Lost Souls, through each and every GhostKidFamily Friday & Chop Up of 2022, through many highs and lows I’ve diamond handed this iconic PFP…

And it’s now no longer mine.

Summary of The Review today:

A Short Story ft. GKD & Anon

A to Z Guide on How to LOAN

Lessons from a Sorrowed Borrower

👻It’s all coming together… JK

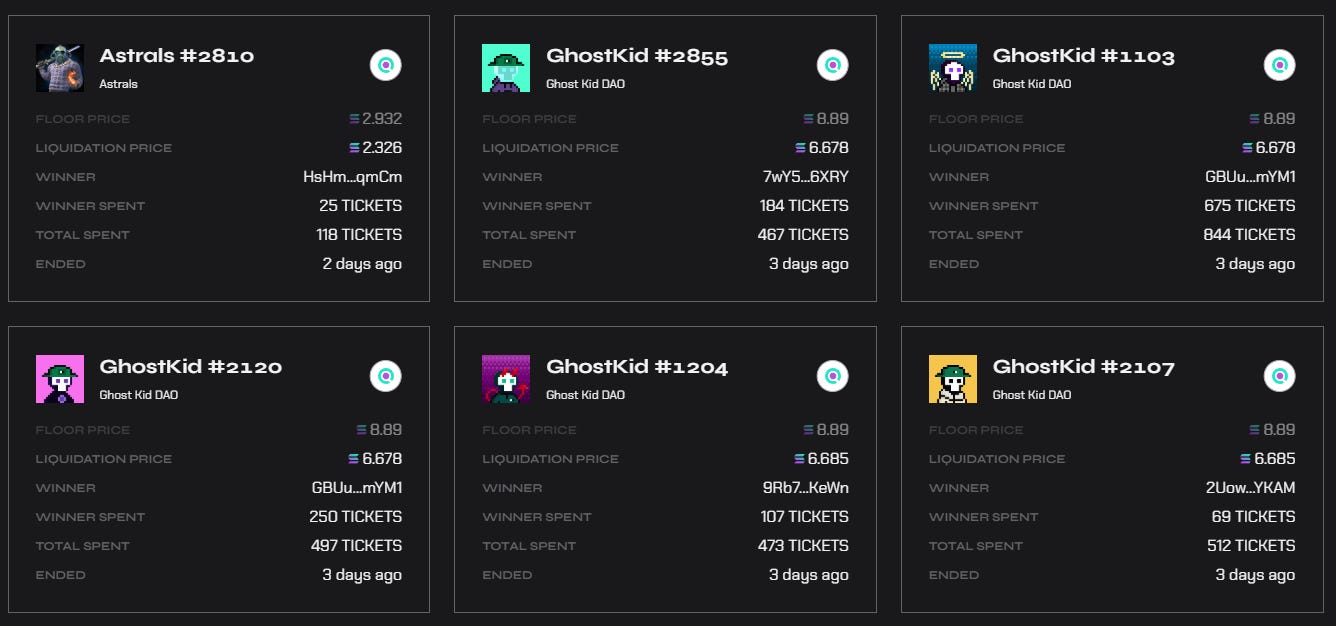

Long story short, this was my mistake, 100%. I loaned my collection of GhostKids out before we broke 10SOL & left them loaned out, collecting debt on the perpetual contracts for each. Over the past few days, SOL rose & GKD ended up falling in combination to an aftereffect of Anon’s mint, to be expected really. It cost me a stack of kids to Frakt’s raffle protocol.

Don’t be fooled, I’m not uninformed. I’ve been a loan-maxi since the jump, an early user of Frakt’s platform & shuffled through the ventures of Pawn Stars, Pawn Shop Gnomies, SharkyFi, Defi Society & more to test the waters of NFT-enabled DeFi.

This was pure negligence. Was this somewhere I’ve messed up before?

Definitely.

Was it because I went in with much hopium & no plan?

Probably.

But will I overcome this challenge & adapt my behavior in the future?

AB-SOL-UTELY!

📈Loans 101

I’ll continue to be a proponent for loans in the future, but like said, this liquidation means NOTHING if I do not LEARN. Class is in session: what are loans & their downsides?

Loans are agreements to borrow; a sum or object to be lent out, majority with interest over the lending period. Pretty straightforward, now the ups and downs:

Downsides:

You can get liquidated for your favorite NFT (if you loan it out)

You’ve got a time limit on the cash (if you take the loan)

You collect interest on NFTs (HIGH interest in conventional terms)

You’re forfeiting capital in exchange for rights to the collateral (as a Lender)

Basically, you’re subject to the protocol & its guidelines.

Upsides are a bit different, but depend more on HOW you’re using the protocol. Lenders reap a lot of these rewards but these serve to a certain caliber of investor. Borrowers experience very little of these.

Upsides:

You can provide liquidity & collect great APY

You can enter liquidation raffles with underlying NFT/token

You’re able to get FAST CASH on your NFT’s value without SELLING

Although Lenders/Holders receive most rewards, the protocol itself normally experiences the safest “passive” income after contracts are complete & secure.

One of the great things about blockchain: these are designed to collect fees for service, in this case, loans.

📚What did I LEARN:

Low risk, High reward - I want to maximize returns, not cripple my portfolio. If possible, be the loaner, never be a borrower.

Remember the Deal - When taking a loan, you’re taking a responsibility to pay back at a later date. Borrow with a plan. When lending, you give up capital in exchange for the rights to collateral OR payment + interest. Make sure that’s a win-win as a lender.

Capital is KING - Although lending is safest, to do effectively you need greater starting money to drive more value back to you.

Loaning your PFP - Don’t do it! Especially if it holds ANY value OR if you’re the sentimental type, don’t chance it. Trust me, I hate to say but this is not even the first time I’ve liquidated my brand PFP

Protocols aren’t Equal - There are MANY loaning services out there, don’t stick just to one. Diversifying is always important in any portfolio, the loan port isn’t different!

Well. Great week ended off on a down note but then again, Anon’s scarf traits are looking clean. Although this is still a huge loss for my journey, it IS a journey. What’s next for the AskNoot Brand, you ask? NO IDEA! We’ll both find out next week.

I’m gonna go take a break from NFTs…

…for like 8 hours.

-Caleb🧣

Caleb! Nooooo! Your pfp was/is your brand!